Contractual Liability – The Crown Jewel of a Contractor’s General Liability Insurance

Hidden within a contractor’s general liability insurance policy is a valuable asset that’s often overlooked—the contractual liability coverage component. This "crown jewel" of your insurance policy is highly coveted by clients, whether they are Owners, General Contractors, or EPC Contractors. But how do they try to extract this jewel for their own benefit, and at your expense?

The Client's Perspective

Clients frequently require contractors, subcontractors, material suppliers, and fabricators to name them—along with a host of others such as agents, subsidiaries, and representatives—as additional insureds on the contractor’s general liability insurance policy. While this seems like a standard request, it’s crucial to understand the client’s motivation behind it.

Why Clients Want Indemnities

Clients often push for broad or intermediate form indemnities in their contracts to transfer financial liability for claims related to bodily injury or property damage—claims often stemming from their own negligence. By doing so, they shift the financial burden and defense costs to lower-tier contractors and suppliers. This makes sense from their perspective, but it creates significant risk for contractors.

A limited form indemnity, which is fairer and more balanced, is now rare. It’s about as common as finding a prehistoric coelacanth in your backyard pond.

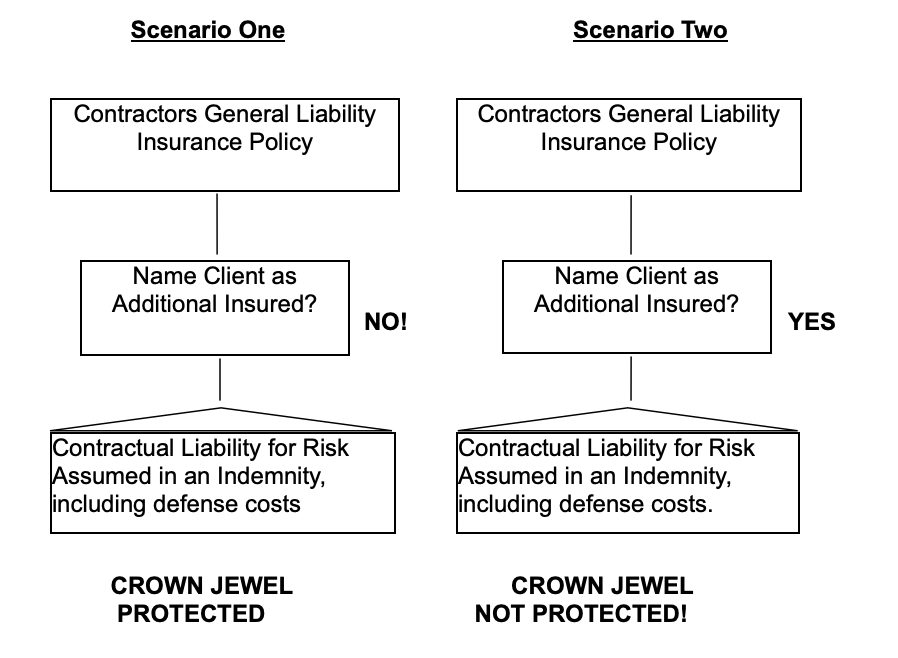

The Difference Between Two Common Scenarios

Let’s look at two scenarios to see how contractual liability plays out:

Scenario One: No Additional Insured Requirement

The contractor agrees to a broad or intermediate form indemnity in the contract but does not name the client as an additional insured on their general liability insurance policy.

In the event of a claim against the client that supposedly arises from the contractor’s work, the client will likely demand indemnity and defense. A savvy contractor will refuse, claiming the issue didn’t arise from their work but from the client’s negligence. The client’s demand for defense costs ends up crumpled and tossed in the trash—game over for the client.

Scenario Two: Additional Insured Requirement

In this scenario, the contractor agrees to both the broad or intermediate form indemnity and to name the client as an additional insured on their general liability insurance policy.

If a claim arises, the client doesn’t need to fight with the contractor. Instead, the client contacts the contractor’s insurance company, demanding an immediate defense and coverage for the claim. Since the client has been added as an additional insured, they receive all the benefits of the policy, including coverage for the financial liabilities and defense costs outlined in the indemnity clause.

To make matters worse, the contractor’s insurance company might end up covering liabilities even when they arise from the client’s sole negligence. That’s because the contractor’s policy includes contractual liability coverage, which extends to the indemnity obligations.

The Costly Difference

Scenario One: No additional insured, and the contractor’s crown jewel—contractual liability coverage—remains protected.

Scenario Two: The client is named as an additional insured, and the contractor’s crown jewel is not protected, leaving the contractor exposed.

Protecting Your Crown Jewel

Contractors should remember that their general liability insurance policy is an asset they pay for, and it should benefit their company, not others for free. By adding a client as an additional insured, contractors risk exposing their coverage to claims arising from the client’s negligence, which can raise premiums or affect policy renewal down the road.

Clients can and should purchase their own insurance to meet their needs. Don’t let them dig into your coverage by naming them as additional insureds on your policy. Protect your company’s assets, and use your insurance for its intended purpose—to cover your risks, not theirs.